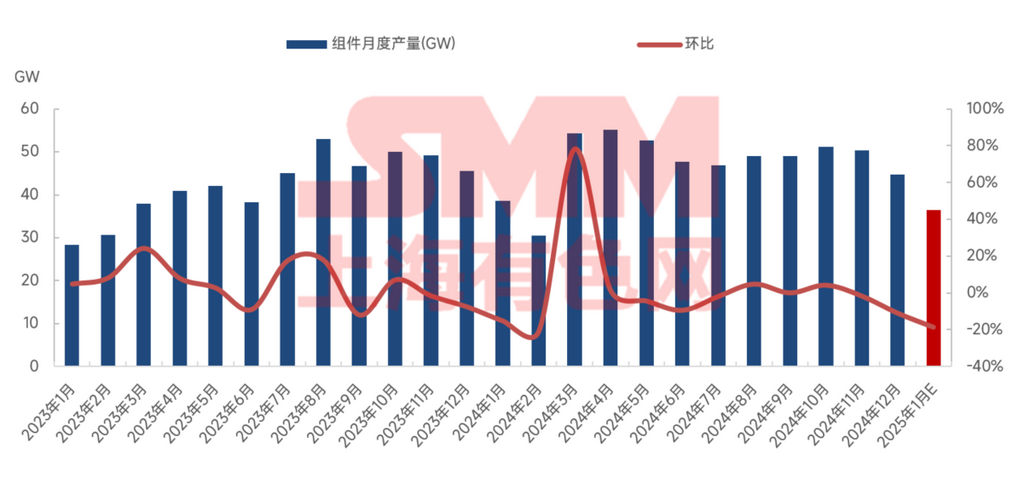

According to SMM statistics, China's PV module production in December decreased by approximately 10.9% MoM, with an industry operating rate of around 44.2%. For the full year of 2024, China's cumulative PV module production is expected to be up about 12.2% YoY compared to 2023. By technology route, TOPCon continues to dominate the mainstream market share, while the production schedule share of BC modules remains stable with slight growth, driven by the push for annual targets at year-end. P-type module production decreased by 29.3% MoM, accounting for 3.6% of total production, while N-type module production decreased by 10% MoM, accounting for 96.4% of total production. The operating rate of PV modules in China in December was approximately 46.7%.

At the year-end, domestic and international demand drivers weakened, leading to a reduction in new orders. Enterprises aimed to control year-end inventory levels by lowering operating rates. Both domestic and overseas production bases of Chinese companies saw reduced output, with many module manufacturers opting to produce based on demand. Operating rates of first- and second-tier top-tier enterprises declined, and the number of top-tier enterprises implementing significant production cuts increased. This was attributed to high-turnover inventory at year-end, the retreat of the peak delivery period for rush installations, reduced export tax rebate rates, and losses caused by cost-price inversions.

Entering January 2025, China's PV module production schedule is expected to continue declining, down 18.7% MoM compared to December 2024, with an industry operating rate of approximately 35.95%. By technology route, P-type module production is expected to decrease by 13.6% MoM, accounting for 3.8% of total production, while N-type module production is expected to decrease by 18.9% MoM, accounting for 96.2% of total production. The operating rate of PV modules in China in January is expected to be around 37.8%.

The primary reduction in January's module production schedule comes from domestic bases of Chinese enterprises. Among overseas bases, facilities in the four Southeast Asian countries have gradually ceased operations by the end of 2024, with companies shifting their module production layout to Indonesia. US bases are also appropriately lowering operating rates due to weakened order demand. In January, the New Year and Chinese New Year holidays reduced the actual number of production days, affecting the planned production volume of each company. According to SMM, module companies generally take 10-15 days off around the Chinese New Year. Many small factories plan holiday breaks ranging from half a month to a month, resuming production only when orders are available. Top-tier enterprises showed a significant reduction in production in January, down 18.6% MoM compared to December. Second- and third-tier enterprises, having already maintained low operating rates for an extended period, have limited room for further production cuts. Each module company formulates its production plan based on its own orders and the visibility of future orders. Most companies, due to the off-season demand and pressure from losses, focus on selling inventory and take extended holidays.

Recently, with the rise in silicon wafer and solar cell prices, module prices also show signs of upward movement. On one hand, rising raw material prices strengthen cost support; on the other hand, market sentiment to stand firm on quotes, coupled with production cuts and inventory control by module companies, has led to plans to raise quoted prices by 0.01-0.02 yuan/W. However, a gap remains between actual transaction prices and quoted expectations. Although top-tier module companies are united in standing firm on quotes and aiming to raise prices, the current domestic Q1 off-season demand, intensified competition in the residential market, and unclear acceptance of price increases in the centralized market suggest that price struggles will persist in the short term. Actual transaction prices for modules are unlikely to rise before and after the Chinese New Year. By the end of Q1, as demand recovers, module prices are expected to stabilize and rise slightly, supported by both cost and demand.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)